Feature

Australia’s iron ore machine faces a structural test

New pressures are forcing a rethink of a model long-defined by scale and efficiency, Alejandro Gonzalez reports.

Main image: Open-pit mining in Australia. Credit: Super8/Shutterstock.com

From the red dust of Western Australia (WA) to the negotiating rooms in Beijing, Australia’s iron ore sector is navigating softer prices, shifting demand and rising competition.

The Pilbara in WA is home to the world’s largest and most economically significant iron ore deposits; the large, dry and sparsely populated region has been a major contributor to global steel production for decades.

Over this time, Australia’s iron ore dominance has been based on extracting high volumes of hematite and moving it efficiently by rail and ship to Asia’s blast furnaces.

That model still delivers. Australia produced 967.8 million tonnes (mt) of iron ore in 2025, up 1.4% year-on-year (YoY), and accounted for 36.8% of global output in 2024, according to a report by MINE's parent company, GlobalData, entitled Australia Iron Ore Mining to 2035.

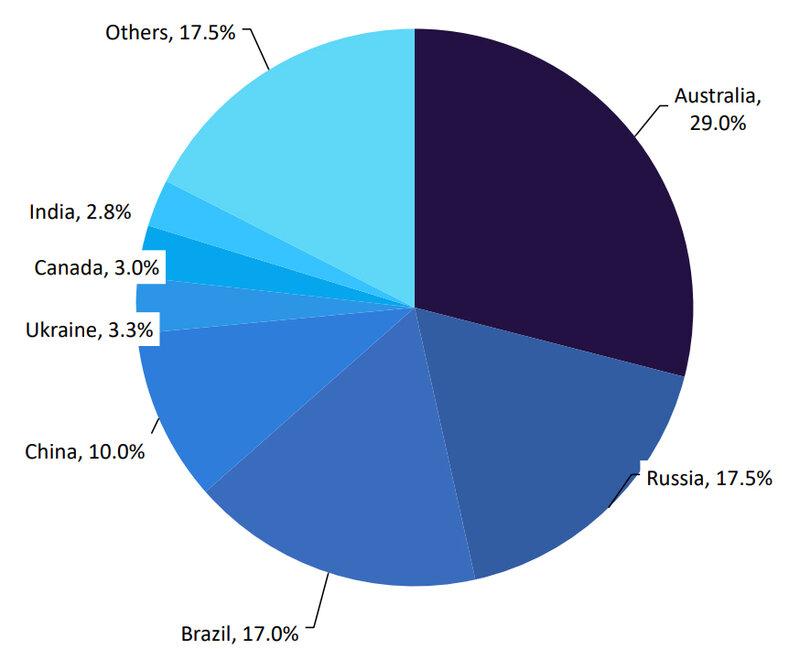

Iron ore reserves by country, 2025. Credit: GlobalData, US Geological Survey.

It exported more than 911mt in 2024, retaining its position as the world’s largest supplier to the seaborne market.

As of January 2025, the country held 29% of global crude ore reserves.

Yet, beneath that operational continuity, market conditions have shifted.

Softer pricing

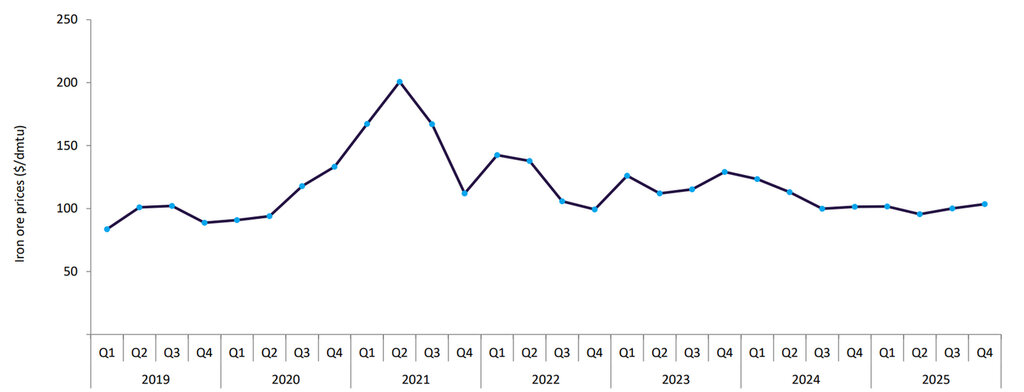

Iron ore prices fluctuated through 2025, averaging $100.2 per dry metric tonne unit (dmtu), down 8.4% YoY, as global steel production moderated and supply increased.

Global iron ore prices, quarterly ($/dmtu), 2019–25. Credit: GlobalData.

The weaker sentiment was driven by reduced steel output in China, elevated supply from major exporters and growing demand for higher-grade, lower-emission feedstock.

China, to which Australia’s iron ore market is closely tied, introduced additional uncertainty in September when its state-owned China Mineral Resources Group instructed steelmakers to avoid imports from BHP’s Jimblebar mine. China had imported 587.3mt of iron ore and concentrates from Australia during the first nine months of 2025, up 1.5% YoY.

These conditions have tightened margins at higher-cost operations, resulting in several operational headwinds and mine closures in Australia last year. In the Pilbara, ramp-down activity at BHP’s Yandi mine reflected resource depletion. Mineral Resources placed its Koolyanobbing operation in WA on care and maintenance in early 2025 due to limited reserves and cost pressures. Output at Roy Hill also softened amid weaker pricing and weather-related disruption including Cyclone Zelia in February.

Despite these pressures, national production volumes proved resilient – a reflection of low-cost scale, established infrastructure and ongoing ramp-ups at newer projects.

Supply replacement and new projects

Closures at Itochu’s Yandi and Mineral Resources’ Wonmunna operations in the Pilbara are expected to remove 27.2mt of supply this year based on 2024 output levels. Resource depletion remains an ongoing challenge across mature hematite deposits.

However, exploration spending signals continued reinvestment.

In 2025, exploration spending in the state surged by 20%, reaching $806m (A$1.14bn), GlobalData reported. This increase was attributed to the strategic need for mining companies to replenish their depleted reserves.

Meanwhile, ramp-ups at several projects are bolstering capacity. Australia’s iron ore output is forecast to increase by 2.6% in 2026 to 993.4mt, supported by continued ramp-ups at the Onslow, Western Range and Iron Bridge (North Star Magnetite) projects.

Additional supply is expected from the planned start-up of McPhee Creek and Lamb Creek, alongside the resumption of operations at the Koolyanobbing mine in December 2025, following the sale of Mineral Resources’ Yilgarn iron ore assets, including Koolyanobbing, to Yilgarn Iron Investments on 30 June 2025.

In addition, the Western Range mine, operated by Rio Tinto (54%) and China Baowu Steel Group (46%), began production in late March 2025, adding 25mt of capacity annually and further strengthening Australia’s supply base, GlobalData reported.

GlobalData reports that, in response to declining ore quality at its ageing mines in WA, Rio Tinto plans to begin blending Australian and African iron ore at Chinese ports from 2026. The approach will combine higher-grade material from Guinea’s Simandou project with Pilbara ore to maintain iron content levels. Rio Tinto has already started port-side blending in China, including material sourced from its Canadian operations.

Australia's iron ore output is forecast to increase by 2.6% in 2026 to 993.4mt.

GlobalData forecasts that Australia’s iron ore exports will grow at a compound annual growth rate of 2.3%, reaching 1.04 billion tonnes by 2030.

According to the Department of Industry, Science and Resources, iron ore export earnings are expected to account for more than 25% of total resource and energy commodity exports over the 2025–26 outlook period. With prices declining, earnings are forecast to fall by $2bn to $114bn in 2025–26, before dropping further to $107bn in 2026–27.

Despite volume growth potential, other structural pressures are afoot.

From ore exports to green iron

A more fundamental question is emerging: should Australia remain primarily a raw ore exporter or move further along the value chain?

According to the World Economic Forum (WEF) in its Unlocking Asia-Pacific as a First Mover: Australia’s Green Iron Opportunity report, Australia faces a structural turning point as East Asia decarbonises and demand shifts towards low-carbon “green iron”.

The report notes that iron ore exports generated A$138bn in 2024, accounting for 21% of Australia’s export earnings. Converting iron ore into low-carbon direct reduced iron (DRI) using renewable energy and hydrogen could lift this figure to around A$250bn annually, while helping to offset expected declines in coal and gas exports, which account for 14% and 10%, respectively.

The paper also highlights that iron and steelmaking contributes 7–9% of global emissions. With the world’s largest iron ore reserves, alongside significant renewable energy potential and established export infrastructure, Australia could export enough green iron to abate up to 4% of global emissions, around four-times its own, if it captured a 40% share of the market.

The proposition is ambitious. Most Australian exports are below typical DRI-grade thresholds without additional beneficiation. Upgrading ore, developing hydrogen supply chains and financing large-scale DRI plants would require substantial capital investment and regulatory clarity. Institutional investors, according to WEF, are awaiting firm offtake commitments and policy support before deploying capital at scale.

Whether these initiatives evolve into a structural shift remains uncertain, but the strategic direction is clear...

Some collaboration is under way. Rio Tinto, BHP and BlueScope are exploring pathways to convert lower-grade ore into DRI-compatible material. Early-stage projects may rely initially on natural gas before transitioning to lower-carbon hydrogen.

Whether these initiatives evolve into a structural shift remains uncertain, but the strategic direction is clear: steel decarbonisation is altering the competitiveness of iron ore.

For now, the Pilbara’s production lines continue to run at scale. Australia retains cost advantages, established logistics and deep integration with Asian steel markets.

Yet, the defining pressures are no longer purely cyclical. Grade quality, emissions intensity, pricing leverage and the green transition are reshaping the competitive landscape.