Feature

Can Australia turn cobalt into a viable battery supply chain?

Australia is advancing cobalt refining, but competing with China’s scale and cost advantages will likely require carving out a narrower, premium niche. Heidi Vella reports.

Main video supplied by Patsperspective/Creatas Video via Getty Images

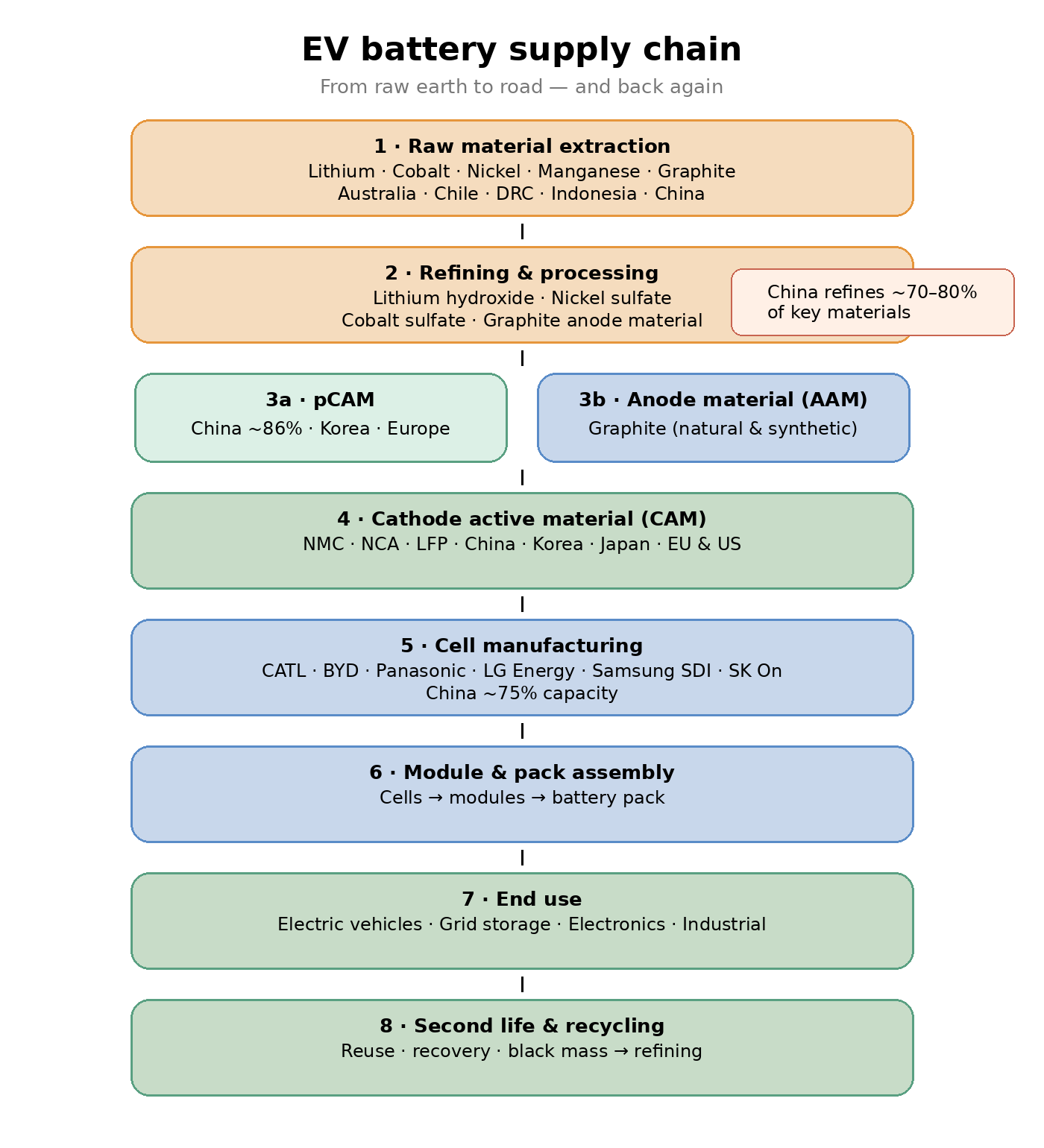

As 2025 drew to a close, after two years of technical tinkering, Australian miner Cobalt Blue Holdings (CBH) met a much-coveted milestone – it produced cobalt sulphate that met the stringent specifications required for Precursor Cathode Active Material (pCAM) manufacturing, a key step in entering battery supply chain qualification processes rather than full commercialisation.

A powdered mix of transition metals, pCAM is crucial for lithium-ion battery cathodes; however, it is only produced by a select, but growing number of producers, outside of China, which currently controls 95% of pCAM capacity, according to the International Energy Agency (IEA). The country also accounts for around 85% of battery-grade cobalt sulphate, according to the US Geological Survey.

CBH’s proprietary flowsheet process for cobalt sulphate, produced at its Broken Hill Technology Centre in New South Wales, aims to produce the same product as Chinese refiners, but uses a salty brine process rather than acids, Joel Crane, business development manager told MINE magazine. Its unnamed Japanese partner confirmed the product met specifications for low trace metal levels, a prerequisite for progressing through multi-year customer qualification cycles.

Joel Crane, business development manager, Cobalt Blue Holdings

“The next step, which is a big one of a long list, is to build the refinery in Kwinana [Western Australia], and then, because it's a different plant, we will have to go through the qualification process all over again,” says Crane.

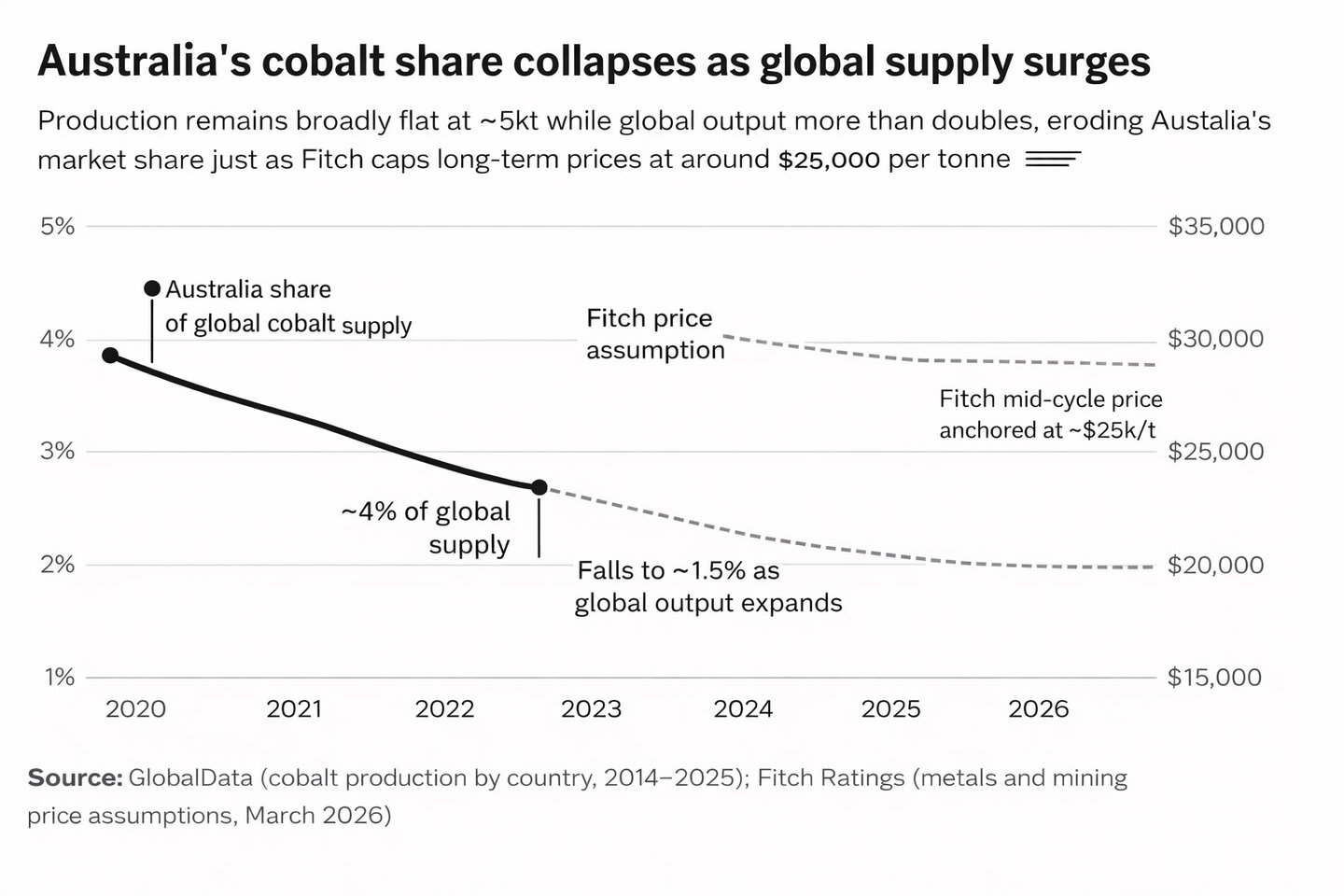

Although there are still hurdles to climb, the milestone sets the firm on the path to final investment decision (FID) on such a plant, while highlighting the gap between technical validation and commercial deployment. It also indicates a successful pivot from cobalt mining to refining. In 2024, the company was forced to abandon its Broken Hill Cobalt Project when global prices fell to historic lows of around $12/lb, driven by production expansions in the Democratic Republic of Congo (DRC) and Indonesia.

This price collapse reflects a structurally oversupplied market, with the Global Cobalt Mining to 2035 report by MINE’s parent company, GlobalData, noting that rapid supply growth from the DRC and Indonesia pushed cobalt prices to multi-year lows, undermining project economics across the sector.

Pursuing pCAM

CBH’s achievements are a tentative win for Australia’s wider bid to build out its battery manufacturing value chain, in which it has invested millions in government funding, although scaling these advances into commercial operations remains uncertain.

Leading these efforts is The Cathode Precursor Production Pilot Plant (C4P), run by the Minerals Research Institute of Western Australia (MRIWA) with Australia’s national science agency, the Commonwealth Scientific and Industrial Research Organisation and Curtin University. It is one of only a small number of facilities globally to pursue pilot production of pCAM, but operates at a scale far below commercial requirements.

MRIWA CEO, Nicole Roocke, tells MINE magazine that the plant allows Western Australia (WA)‑based researchers to move beyond the laboratory and generate the practical data that industry requires before committing to large‑scale investment, particularly around process stability and impurity control.

Associate Professor Laurence Dyer from the WA School of Mines at Curtin University, notes that producing battery-grade material requires extremely high purity levels and tight process control, reflecting a shift from mining into advanced materials processing.

Currently, researchers at the plant are tweaking formulations and testing impurity tolerance while lowering costs, both critical for commercialisation but difficult to achieve outside China, where scale, integration and cost efficiencies are already established.

As Usha Haley of the Stern School of Business at New York University, an expert on China, green tech and mining, explains, for Australia, building competitive cobalt refining, and pCAM production from scratch means competing against China, which has “simultaneously funded the technology, written the standards, and engineered the dependencies.”

Laurence Dyer, Associate Professor, WA School of Mines at Curtin University

TowHaul Lowboys utilize a single, haul-truck type axle. TowHaul offers a dry drum brake configuration or a wet brake configuration with TowHaul’s patented Brake Cooling System.

Frank Smith, Founder and CEO of TowHaul

“Subsidy-driven under-pricing and technology investments have created technical barriers in hydrometallurgical refining, solvent extraction and the nanoscale purity demands of electric vehicle (EV) battery manufacturers to discourage parallel development elsewhere,” she says, pointing to structural rather than purely technological barriers.

Haley adds that Australia's structural vulnerabilities include high labour costs, fragmented regulatory frameworks, limited domestic demand and capital markets oriented toward short investment horizons, all of which affect project bankability.

These constraints are reinforced by broader industry trends identified in GlobalData's Australia Mining Review 2025 report, which highlights rising labour costs, regulatory complexity and environmental, social and governance compliance burdens as persistent cost pressures across the sector, further widening the gap with lower-cost refining hubs.

“These become higher barriers when the benchmark competitor operates outside normal market disciplines and steers global technology trajectories to sustain its dominance,” she says.

Managing risk and markets

Roocke says C4P doesn’t attempt to “replicate China’s manufacturing scale” but instead “supports early‑stage capability development and technical understanding”, reflecting a strategy focused on niche capability rather than direct competition.

However, Dyer acknowledges the wider challenges stemming not just from China’s dominance but Australia’s ‘dig and ship’ mentality which has seen manufacturing capability lost over the decades, limiting downstream industrial depth.

“Making a high purity product is not the mining company's core business; you need 99.99% purity, which veers into the material science space, in addition to really tight controls on your processes,” he explains.

Building up a value chain takes “a huge amount of investment”, he adds, with recent commodity price volatility weakening investor confidence in downstream processing projects.

The C4P plant was originally set up through the industry-academia-government-funded Future Battery Industries Cooperative Research Centre. It was intended that technology developed from the pilot project would form the basis for an intellectual property licence to scale up the process, but the crashing nickel price in early 2025 “killed much of that off”, says Dyer, highlighting the sector’s exposure to commodity price volatility.

Chile’s President Jose Antonio Kast speaks during his visit to the Industrial and Mining Training Center (CEIM) in Antofagasta, Chile on March 17, 2026. Credit: SEBASTIAN ROJAS ROJO / AFP via Getty Images

That volatility is not isolated. The Australia Mining Review 2025 report notes that weakening prices and demand uncertainty across battery metals have already disrupted investment pipelines, reinforcing the financial fragility of downstream processing projects.

The risk for investors is perceived as high because processes need to be proven again at scale and the C4P pilot plant is focused on a nickel-cobalt-manganese mix, creating a concern that the chemistry pathway could be replaced by another, such as shifts toward alternative cathode chemistries.

This risk is compounded by longer-term technological shifts: the Global Cobalt Mining to 2035 report highlights a gradual move towards low-cobalt and cobalt-free battery chemistries, which is expected to reduce cobalt intensity and cap future demand growth.

US investment

There is movement with investments, however, despite the downturn. Major Japanese mining company Sumitomo Metal Mining has invested in The Kalgoorlie Nickel Project, a major Western Australian nickel-cobalt development by Ardea Resources, that is believed to hold 437 million tonnes of resource, making it one of Australia's largest high-grade nickel-cobalt deposits, although development timelines remain long.

Australian company Lynas Rare Earths has inked a $137m (A$197.77m) deal with US President Donald Trump’s Department of War (formerly the Department of Defense). It is also backing a consortium to acquire a 40% stake in Glencore’s cobalt mines.

The deals are giving hope to CBH’s refinery plans. To secure investment the project needs new offtake partners – banks typically require 60%-80% offtake in place and its current partner has signed up for only 30%, underscoring financial constraints tied to market demand. The company is in “advanced discussions” with others, according to Crane.

The product will be cost comparable with Chinese supply, Crane says, but acknowledges a “chicken and egg” problem around proving viability before securing finance.

The company had hoped to be in a position to secure finance by the end of last year but was held back by volatile markets and changing government policy.

“When we started this journey… the demand was not so strong,” Crane says, citing the reversal of the Inflation Reduction Act.

“No one is willing to put down the money… our customers aren’t telling us to buy non-China supplies,” he adds, highlighting weak willingness to pay a premium.

Another challenge has been the lacklustre demand for EVs, which has moderated short-term growth expectations for battery materials. However, Crane says there is potential for Australian and US government funding; the former is expected to back a loan for half the money, and the company is in “deep discussions” with the latter.

It hopes to be a beneficiary of the US Government’s latest funding ($500 million) for critical minerals. Crane says it could access this through its now US-backed feedstock supplier Glencore – overall it hopes to reach FID by the end of this year, contingent on financing and offtake alignment.

Alongside producing cobalt sulphate from raw feedstock, the company is also pursuing black mass recycling, which Crane says can work similarly to other feedstocks but is a much “trickier” market because it requires population density and high recycle rates, which Australia doesn’t have.

“We are just exploring it as an alternative, with it making up potentially 10-20% of the overall shared feedstock,” he says.

Australia’s eye is on the prize

Dyer questions whether Australian production of pCAM could ever be cost comparable with Chinese production – “I don’t think it is physically possible” – but he believes it is more important to produce material that will sell at a sustainable price, even if that implies a structural problem.

“It will require a premium… but there appears limited willingness to pay for supply chain diversification in practice,” he says.

However, there is a concerted effort in Australia to build the industry, although policy support alone may not offset cost disadvantages.

Chile’s President Jose Antonio Kast speaks during his visit to the Industrial and Mining Training Center (CEIM) in Antofagasta, Chile on March 17, 2026. Credit: SEBASTIAN ROJAS ROJO / AFP via Getty Images

Meanwhile, the Australian Government is actively attracting investment in the critical minerals sector through the Critical Minerals Strategy 2023–2030 and the Future Made in Australia plan.

These efforts align with incentives highlighted in the Australia Mining Review 2025 report, including tax credits for processing and refining, but their impact will depend on whether they can offset structural cost disadvantages and weak market signals.

Overall, while Australia is advancing technical capability in battery materials, the decisive constraints remain economic, structural and market-driven rather than purely technological.