Feature

Technology targets a revival in copper refining

With smelting capacity tightening and demand rising, Australia's processing capacity is under strain, one that emerging technologies may help address. Scarlett Evans reports.

Main video supplied by SVTeam/Creatas Video+ / Getty Images Plus via Getty Images

Australia is home to some of the world’s largest copper reserves, with the US Geological Survey (USGS) reporting that the country houses some 100 million tonnes (mt) of the mineral (just over 10% of global supply). Yet as copper demand rises, Australia’s ability to process copper domestically – particularly at the smelting stage – is coming under pressure.

Processing remains heavily concentrated in China, Japan and South Korea, leaving Australia reliant on export markets for refining, a model that is under renewed scrutiny as electrification drives demand for finished copper products.

According to Australia Copper Mining to 2035, a report by MINE's parent company, GlobalData, the country has a limited number of smelting and refining facilities and remains highly export-oriented for copper ores and concentrates.

USGS data suggests a more nuanced picture. Australia produced roughly 800,000t of copper in 2024 and refined around 460,000t domestically, placing it between export-led producers such as Peru and more integrated systems such as Canada.

The issue is not the absence of refining capacity but rather its scale and trajectory.

More critically, Australia’s copper value chain is becoming unbalanced: smelting capacity is tightening, while downstream refining capacity remains in place.

This imbalance is widening. GlobalData forecasts copper demand will reach 35.1mt by 2030, driven by electrification, while supply growth is increasingly concentrated in regions such as Chile, Peru and the Democratic Republic of Congo – but not Australia.

That structural dependence is now being tested. Pressure on Glencore’s Mount Isa smelter, one of the country’s few remaining smelting hubs, has exposed how little redundancy exists in Australia’s upstream processing system.

While government support has delayed its closure, the underlying trajectory is unchanged: capacity is tightening, not expanding.

GlobalData figures indicate that Australian copper output declined in 2025, leaving it out of step with modest global supply growth and reinforcing the country’s weakening relative position. The immediate question is how to replace that capacity. The harder one is whether it can be replaced on competitive terms.

Jose Domingo Villanueva

It comes at a moment of sharp contradiction. Mining remains central to the economy, accounting for around 11.6% of gross domestic product in 2025, yet foreign direct investment (FDI) into the sector fell 28.7% year-on-year in 2024, according to a report by Mining Technology’s parent company, GlobalData, entitled Chile Copper Mining to 2030, suggesting that capital is already pricing in regulatory risk. At the same time, mining exports reached $63.3bn (58tn pesos) in 2025, around 59% of total exports, underlining the sector’s continued macroeconomic weight.

For a country that remains the world’s largest copper producer, responsible for roughly 23% of global output, and a central player in lithium, the issue is not resource endowment. It is the ability to execute projects within a predictable time frame.

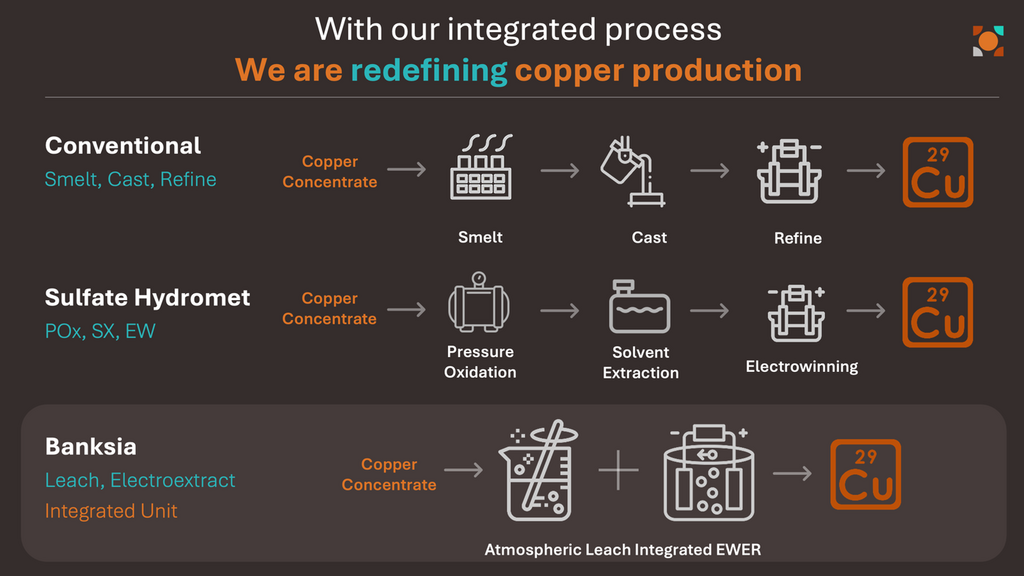

Copper processing pathways: pyrometallurgy vs hydrometallurgy

Traditional smelting and refining separates copper production into multiple high-temperature stages, while hydrometallurgical approaches aim to produce cathode directly through solution-based processing.

Source: Banksia Minerals

Copper without the furnace

In this context new approaches are emerging.

Brisbane-based start-up Banksia Minerals is commercialising technology developed by the University of Queensland (UQ) that aims to reduce the cost and energy intensity of copper processing through a hydrometallurgical route.

Backed by a A$5m (£2.6m) grant from the Australian Renewable Energy Agency (ARENA), the company is targeting a pilot plant by 2028, placing it firmly in the demonstration phase rather than commercial deployment.

“Pyrometallurgy… is optimal when you have a nice high-grade concentrate feed,” says James Vaughan, leader of the Hydrometallurgy Research Group at UQ, “but as we globally use up high-quality ore, we are going to need something different.”

This “something different” is not a new concept, but Banksia claims to have resolved a long-standing barrier.

At a process level, Banksia replaces conventional smelting with a direct leach–electrowinning (EW) pathway. The flowsheet avoids solvent extraction, with purification achieved through a downstream refining stage capable of producing LME Grade A cathode. This configuration opens a retrofit option, decoupling the process into leach–EW–electrorefining (ER) stages that can be integrated with existing refinery assets.

Chloride-based hydrometallurgy has been studied for decades, with well-understood theoretical advantages: lower operating temperatures, reduced emissions and safer working conditions. The reason it never reached commercial scale came down to a stubborn problem at the recovery stage. When copper was extracted from the solution electrically, it formed as a granular, sandy material that was commercially useless.

“The breakthrough[…] was enabling smooth copper plating from a chloride leach,” says Banksia CEO Leigh Staines. “That effectively unlocks a pathway that has been understood for decades but never fully commercialised.”

Improved impurity handing is another benefit. “Banksia’s technology doesn’t cause certain minerals to react, that in a smelter would react automatically – meaning we avoid unnecessary waste generation," Vaughan says.

If scalable, the process could bypass smelting entirely, producing cathode directly and collapsing the traditional smelting-refining chain into a single step. However, significant challenges remain before that becomes viable.

Even if the chemistry holds, the economics remain uncertain. Refining is not constrained by technology alone but by energy pricing, scale economics and integrated supply chains.

Industry analysis notes that smelting remains one of the most competitive parts of the copper value chain, with capacity concentrated in regions able to operate at scale and lower cost.

There are also unresolved technical constraints. Chloride systems are inherently corrosive, increasing materials requirements, while reagent will directly affect operating costs. Impurity handling, particularly arsenic stabilisation, shifts risk from emissions to waste management and permitting.

These constraints have historically limited chloride leaching to pilot-scale deployment.

At the same time, investment has not disappeared entirely.

In January 2025, BHP awarded contracts tied to a proposed expansion of its South Australian smelter and refinery operations, suggesting refining remains viable but primarily for large, integrated operators with access to capital and infrastructure.

TowHaul Lowboys utilize a single, haul-truck type axle. TowHaul offers a dry drum brake configuration or a wet brake configuration with TowHaul’s patented Brake Cooling System.

Frank Smith, Founder and CEO of TowHaul

TowHaul Lowboys utilize a single, haul-truck type axle. TowHaul offers a dry drum brake configuration or a wet brake configuration with TowHaul’s patented Brake Cooling System. Using a single axle eliminates tire “skidding” often found with multi-axle trailers when turning on a sharp corner. This “skidding” can cause tire and axle damage leading to downtime. Recognizing the variety of conditions in which mines operate, TowHaul has designed specific lowboy configurations tailored to operate more effectively in specific areas. For example, there are several TowHaul Lowboys currently operating in the unique conditions found in the oil sands of northern Alberta designed with a specific Oil Sands Configuration.

To cope with the extreme ambient temperatures found in Western Australia, TowHaul upgraded the patented Brake Cooling System for our 450-ton capacity lowboys to improve the cooling of the oil in those systems.

Refining economics: scale still wins

GlobalData identifies nearly 90 copper development mining projects expected to come online by 2030, reinforcing that supply growth is being driven by large-scale, capital-intensive developments rather than decentralised processing models.

Copper prices were already volatile through 2025, ranging between roughly $8,500/t and more than $10,000/t, before spiking to nearly $13,000/t and slipping back to around $12,000/t by early April 2026 on the London Metal Exchange, as geopolitical tensions, including the conflict between the US -Israel and Iran, added further instability, hardly a stable basis for long-term refining investment.

China refines far more copper than it mines, importing concentrate at scale, while Japan and South Korea operate as dedicated refining hubs. Resource-rich exporters such as Peru remain export-oriented, while Indonesia has expanded downstream processing through policy intervention.

Australia sits between these models - retaining partial refining capacity but without the scale of global hubs or Indonesia’s policy-driven approach.

Mount Isa has become the focal point of this debate. “Mount Isa was not just a mining operation, it was a major processing hub,” says GlobalData analyst Sai Dheeraj Karanam, pointing to its role in underpinning domestic capacity.

The future of the Mount Isa smelter remains uncertain but no longer immediate. In October 2025, Glencore secured a A$600m government support package to keep the smelter and Townsville refinery operating until at least 2028.

The agreement provides a short-term bridge rather than a long-term solution. Without support, Glencore says the assets would move into care and maintenance.

For regional stakeholders, the challenge is immediate.

Speaking to MINE, Mount Isa mayor Peta MacRae says “one of the biggest challenges we face is energy. The cost of gas is extremely high, and many of our smaller mines rely on diesel generators or gas-generated power — at roughly three times the cost of the National Electricity Market.”

A smaller, deployable processing unit could, she says, also reduce reliance on transporting raw materials over long distances. “It could be a game changer for smaller operations,” she adds.

Energy cost is not a marginal issue, it is central to whether any replacement technology can operate competitively.

The economics of the bailout are instructive. Glencore has cited weak smelting charges and intensified global competition, particularly from China’s expanding processing capacity, as key factors undermining viability.

Energy costs in north-west Queensland are significantly higher than in competing jurisdictions.

GlobalData attributes part of Australia’s production decline to falling grades and transitional mine phases, suggesting that constraints extend beyond processing into upstream supply quality.

As smelting capacity declines, the link between mining and refining weakens, raising questions over how remaining refineries will secure feedstock.

Banksia’s modular model could, in theory, reduce transport costs and enable smaller-scale deployment.

However, the Mount Isa case illustrates the scale of the challenge: even existing, fully integrated infrastructure requires sustained public support to remain operational.

In that context, the question is not simply whether new technologies can replace lost capacity – but whether they can operate without similar forms of support.

Retrofit or rebuild?

Any transition pathway must also account for existing infrastructure, particularly the Townsville copper refinery.

Operated by Glencore, the facility refines anode copper into cathode and has historically depended on feedstock from Mount Isa. This refining stage depends on smelters to supply anode copper, linking its viability directly to upstream smelting capacity. With smelting under pressure and refining still operational, the system is becoming unbalanced.

In this context, several configurations are possible for Banksia; retrofitting the Townsville refinery site to include its technology, deploying its tech closer to the mine then sending material to Townsville for refining, or a hybrid approach combining both.

“The original patented breakthrough centres on a single system that both extracts copper from solution and purifies it to market-grade quality,” Staines said. “Technically, it’s an elegant, end-to-end replacement for both smelting and refining. However, scaling that into a commercial facility would require building entirely new infrastructure from scratch.”

A faster and simpler option is to decouple the process, replacing the smelting function while retaining the refinery. The commercial implications are significant. Rather than billions, a retrofit could be delivered in the hundreds of millions, dramatically reducing both the capital requirement and the execution timeline.

It also lowers risk by building on existing supply chains, and could provide a model for repurposing infrastructure both across Australia and abroad.

“Many jurisdictions are looking to regionalise supply chains and reduce reliance on concentrated processing hubs,” Staines added. “If we can demonstrate success in a case like Mount Isa, it provides a blueprint for deployment in other regions facing similar challenges around infrastructure, supply chains, and energy transition.”

Banksia’s proposed pathway, retrofitting existing infrastructure rather than replacing it entirely, addresses capital intensity but not necessarily operating cost. Lower capital expenditure reduces entry barriers, but operating costs determine viability.

For hydrometallurgical systems, this introduces a trade-off: while they avoid high-temperature furnaces, they rely on continuous electrical input. In high-cost energy environments, the advantage over conventional smelting may narrow.

Without competitive operating costs, modularity alone is unlikely to shift the economics.

“Without coordination between authorities, even good reforms will have limited impact. What Chile ultimately needs is a ‘single window’ approach to permitting and greater clarity regarding the requirements and processing times,” Villanueva adds.

Correa makes the same point more directly. “Administrative correction is the fastest lever available. If Sernageomin defines criteria and the SEA filters inputs properly, you reduce uncertainty without changing the law.”

The government’s creation of a dual Ministry of Economy and Mining, led by Daniel Mas (former head of Consejo Minero, a trade body), consolidates decision-making and may help address fragmentation at the top of the system, says Correa.

Whether that translates into more consistent outcomes remains uncertain. The underlying risk is that institutional incentives, rather than formal structures, continue to drive delay.

More copper, same bottleneck

The timing is not incidental. According to GlobalData, copper production is expected to fall in the near term before recovering and longer-term output could grow significantly towards 2035, while exports of concentrates are expected to continue expanding.

Globally, however, supply is expected to grow at a compound annual growth rate of 4.3% to nearly 29mt by 2030, with expansion concentrated outside Australia.

Global copper demand continues to rise, supported by electrification and infrastructure build-out. This creates a structural divergence: Australia will produce more copper but capture less of its value.

Banksia’s technology sits at the intersection of ambition and constraint. It offers a potential pathway, but not yet a proven one. The key questions are whether it can scale beyond a pilot plant into industrial deployment; whether lower energy intensity can translate into genuine cost competitiveness in high-cost environments; and whether it can integrate into supply chains that have been built around established smelting hubs over decades. The conflict in the Strait of Hormuz brings added pressure to energy and input costs.

Australia’s refining challenge is not a lack of ideas; it is whether any of them can overcome the structural realities that pushed processing offshore in the first place.