Covid-19 briefing

Powered by

Download GlobalData’s Covid-19 Executive Briefing report

- ECONOMIC IMPACT -

Latest update: 18 August

After downturn for several months, positive GDP growth is forecast in all countries.

Polls show that concern over the spread of Covid-19 is increasing, while business optimism remains volatile.

5.88%

Taiwan's real GDP is forecast to grow at its fastest pace in over a decade, by 5.88% in 2021.

2.3%

China’s real GDP is forecasted to expand by 2.3% over the previous quarter in Q3 2021.

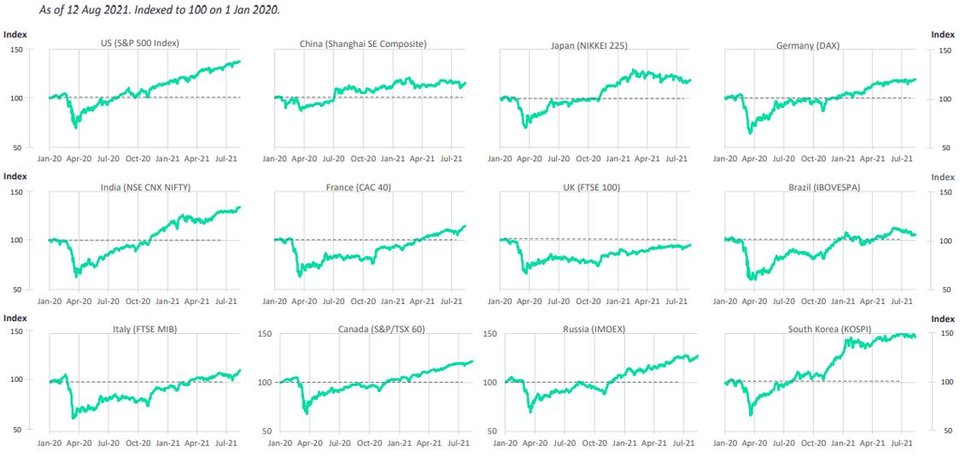

Impact of Covid-19 on equity indices

- SECTOR IMPACT: MINING -

Latest update: 4 August

COAL

ICE Coal Futures prices rose over the course of July, up by 16.4% for the month and were $149.75/t by month end. Prices have been helped by rising demand from China and other parts of North Asia, as well as supply constraints. China's aversion to buying coal from Australia is also leading to high price increases for lower quality coal from markets such as Indonesia.

PRECIOUS METALS

After passing $1,900/oz in late May, the gold price declined in mid-June before steadily improving during July, ending on $1,817/oz. An improving economic outlook had dampened prospects for a rise in the gold price, although they are being supported by continued low interest rates in 2021 and rising US inflation.

BASE METALS

With rising inventories, the average copper price in July was 1.9% down on the June average, although the price improved towards the end of the month, finishing at $9,747.5/t. Concerns over supplies from Chile, where production declined YoY in Q1, plus a threat of strikes as well as higher mining taxes in Peru, may keep prices high over the remainder of 2021.

IRON ORE

The average iron ore remained stable at over $210/t in July, rising marginally by 2.2% versus June and averaging $216.3/t. However, prices are expected to drop as China restricts output from its steel sector. China is aiming to reduce its carbon footprint, with reduced steel output in 2021 to support this. However, to date steel production has increased with output up by 8.3% in Q2 2021 YoY.

PALLADIUM & PLATINUM

After reaching a six-year high of $1,325/troy oz in February, the price of platinum stabilised from March to May before dropping over June and July to its lowest point since January. However, in 2021, prices will be supported by improved demand from the auto and industrial sectors, albeit balanced by significant growth in supply after the 2020 challenges.

Share this article